1. Net Present Value (NPV) & Internal Rate of Return (IRR)

Net present value (NPV) is the difference between the present value of cash inflows and the present value of cash outflows of an investment.

To solve a NPV problem, you just need to find the present value of all the cash flows from the investment. The sum of all these present values is the Net present value of the investment

Example: Calculate the NPV of an investment project with initial cost of $4 million and clash flows for the next 5 years as follows:

year 1: $900,000

year 2: $1.2 million

year 3: -$500,000

year 4: $700,000

year 5: $2 million

Given the discount rate of the project is 11%

NPV = -4 + 0.9/1.11 + 1.2/1.112

+ (–0.5)/1.113 + 0.7/1.114 + 2/1.115 = –$0.9328

million = –$932,800

This project has a negative Net Present Value

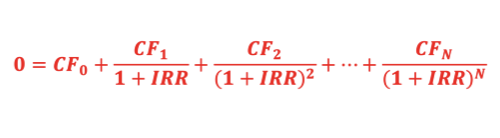

Internal Rate of Return (IRR) is the rate of return that makes the net present value of all cash flows from a particular project equal to zero. In other words, it makes PV of inflows = PV of outflows.

Let r be the required rate of return of an investment, if:

- r < IRR gives NPV > 0

- r > IRR gives NPV < 0

NPV Decision Rule

- Accept the project with NPV > 0

- Reject the project with NPV < 0

- When only 1 of the projects can be accepted, choose the project with higher positive NPV

IRR Decision Rule

- Accept projects with IRR > r (investors' required rate of return)

- Reject projects with IRR < r

*** When NPV and IRR rules give conflicting decisions, always go for the project with the greatest NPV

2. Holding Period Return, Money-weighted and Time-weighted rates of return

Holding Period Return (HPR) is the percentage change in the value of an investment over the period it is held. If the assets have cash flows such as dividends, the return, including these cash flows, is called Total Return.

HPR =

(P1 – P0

+ D1)/P0

P0 = the initial investment

P1 = price received at the end of the holding period

D1 = cash paid by the investment by the end of the holding period

Example:

a. A share of stock is purchased at $50 & sold for $60 six months later. Calculate HPR.

b. Consider the same stock, this time, during the 6-month period, it paid $2 in dividends.

a. HPR =

(60 – 50)/50 = 20%

b. HPR = (60 – 50 + 2)/50 = 24%

Money-weighted Rate of Return is another name for the Internal Rate of Return (IRR). To solve the Money-weighted rate of Return problem, solve the following equation:

PV (outflows) = PV (inflows)

Example: Consider an investment that cover a duration of 2 years. At time t = 0, an investor bought 1 share at $200. At time t = 1 he bought another share at $225. At the end of the second year (t = 2), he sold both shares for $235 each. During both years, the stocks paid per-share dividends at $5. the dividends are not reinvested

We first need to identify cash outflows and inflows

Outflows:

at t = 0, $200 to purchase the first share

at t = 1, $225 to purchase the second share

Inflows:

at t = 1, $5 dividend from the first share

at t = 2, $10 dividend from the 2 shares

at t = 2, $470 from selling both shares

Let r be the money-weighted rate of return

PV (outflows) = PV (inflows)

200 + 225/(1+r) = 5/(1+r) + (470+10)/(1+r)2

Through trial and error, we get r = 9.39%

Time-weighted Rate of Return measures compound growth . It is the rate at which $1 compounds over a specified performance horizon. To solve for the annual time-weighted return, follow these steps:

- Step 1: Price the portfolio immediately prior to any significant addition or withdrawal of funds. Form subperiods based on the cash inflows and outflows.

- Step 2: Calculate the HPR on the porfolio for each sub period.

- Step 3: Compute the product of (1+HPR) for each subperiod to get total return for the entire measurement period

i.e., (1+HPR1) x (1+HPR2) x ... x (1+HPRN)

If the total investment period is greater than 1 year, you must take geometric mean of the measurement period return to find the annual time-weighted rate of return

Example: an investor purchased a share of stock at t = 0 for $100, at the end of next year t = 1, he bought another for $120. At the end of t = 2, both shares are sold for $130 each. Dividend for each of the stock in year 1 and 2 is $2 per share. Solve for the annual time-weighted rate of return for this investment.

Step 1: Break the evaluation period (2 years) into subperiods based on timing of chas flows:

Holding Period 1

Beginning value = $100

Dividends paid = $2

Ending value = $120 (this is the value of the first share at after 1 year)

Holding Period 2

Beginning value = $240 (2 shares, $120 each)

Dividends paid = $4 ($2 per share)

Ending value = $260 (2 shares)

Step 2: Calculate HPR for each period

HPR1 = [(120 +

2)/100] – 1 = 22%

HPR2 = [(260 +

4)/240] – 1 = 10%

Step 3: Find the compound annual rate that would have produce a total return equal to the return on the investment over 2-year period

(1 + time-weighted rate of

return)2 = (1.22)(1.10)

Since the investment period is 2 years long, we have take geometric mean of the result above to get the time-weighted rate of return.

[(1.22)(1.10)]0.5 – 1 = 15.84%

3. Bank Discount Yield (BDY), Holding Period Yield (HPY), Effective Annual Yield (EAY), and Money Market Yield

T-bills are quoted on bank discount basis, which is based on the face value of the instrument instead of the purchase price. The Bank Discount Yield (BDY) is computed as follows:

Note that a yield quoted on a bank discount basis is not representative of the return earned by an investor.

Example: calculate BDY for a T-bill priced at $96,500, with a par value of $100,000 and 120 days until maturity

rBD

= 3,500/100,000 x 360/120 = 10.5%

Holding Period Yield (HPY) is the total return an investor earns between the purchase date and the sale or maturity date. Formula for Holding Period Yield is exactly the same as Holding Period Return (HPR) in section 2.

HPY =

(P1 – P0

+ D1)/P0

P0 = the initial investment

P1 = price received at the end of the holding period

D1 = cash paid by the investment by the end of the holding period

Effective Annual Yield (EAY) is an annualized value, based on 365-day year, that accounts for compound interest

EAY

= (1 + HPY)365/t – 1

Example: Calculate EAY for a T-bill priced at $96,500, with a par value of $100,000 and 120 days until maturity.

HPY

= (100,000 – 96,500)/96,500 = 3.6269%

EAY = (1.036269)365/120

– 1 = 11.45%

Money Market Yield (or CD Equivalent yield) = annualized HPY, assuming 360-day year

Bond Equivalent Yield refers to the 2 x semiannual discount rate. This stems from the fact that yields on US bonds are quoted as twice the semiannual rate because coupon is paid in 2 semiannual payments

Example 1: a 3-month HPY of 2%. Find yield on bond-equivalent basis.

Step 1: convert 3-month yield to effective semiannual yield:

1.022

– 1 = 4.04%

Step 2: double it to get the bond-equivalent yield 2 x 4.04 = 8.08%

Step 1: Convert effective annual yield to effective semiannual yield:

1.080.5

– 1 = 3.923%

Step 2: double it 2 x 3.923 = 7.846%

No comments:

Post a Comment